.svg)

Input Service Distributor vs Cross Charge Explained

In the evolving landscape of GST compliance, businesses with multiple units under the same PAN must grasp the nuances between Input Service Distributor (ISD) and Cross Charge. The distinction is no longer just about tax efficiencies, it's a regulatory imperative. With provisions for ISD becoming mandatory from April 1, 2025, understanding these mechanisms is crucial to avoid penalties and maintain seamless Input Tax Credit (ITC) flow.

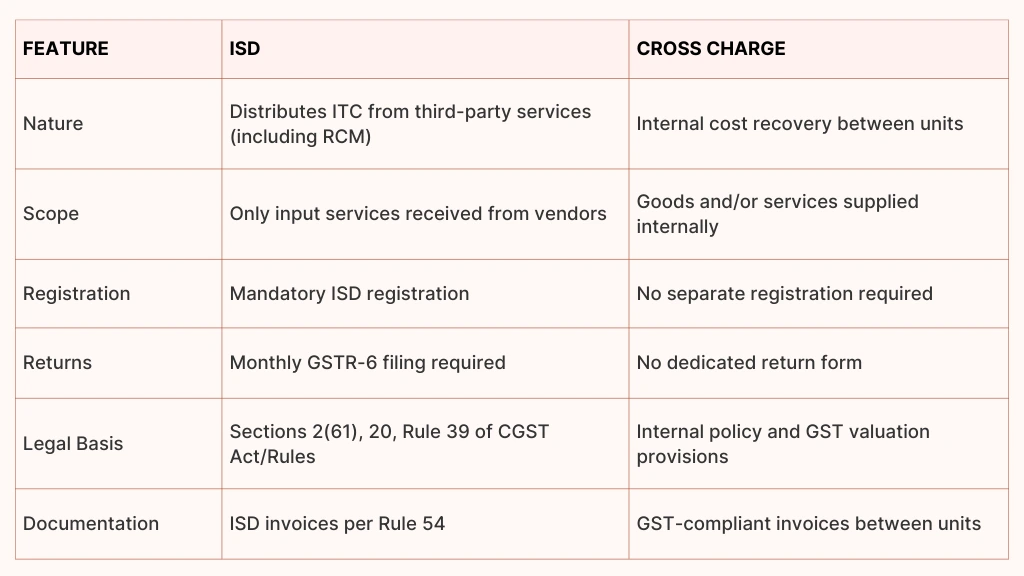

Input Service Distributor (ISD)

An ISD is an office of a supplier that receives tax invoices for input services and distributes ITC to its various units (distinct persons) under the same PAN, as per Section 2(61) and Section 20 of the CGST Act. From April 1, 2025, ISD registration became compulsory.

Cross Charge

Cross charge refers to internal invoicing between units or branches (with same PAN but different GSTINs) for services or goods supplied internally. It’s a mechanism used to recover costs but isn’t governed by ISD-specific provisions.

Key Differences at a Glance

Recent Legal & Regulatory Updates

From April 1, 2025, businesses must register as ISDs if they receive shared services or invoices on behalf of their branches. The changes also mandate ITC distribution through ISD for reverse-charge transactions, a departure from earlier practices where such distribution was optional.

Compliance Mechanics

For ISD (With GSTR-6)

ISDs are required to file Form GSTR-6 monthly by the 13th of the following month. This form captures details of ITC received, eligible vs ineligible ITC, distribution to recipients, amendments, credit/debit notes, and any late fee payable.

Key elements:

- Form GSTR-6 includes tables:

- Table 3: Inward ITC received

- Table 4: ITC available and eligibility

- Tables 5 & 8: Distribution to units

- Tables 6A/6B: Amendments and notes

- Table 9: Redistribution

- Table 10: Late fee and related details

- Table 3: Inward ITC received

- It’s mandatory to file even if ITC to distribute is zero you must submit a “Nil” return.

- Filing is available via the GST Portal under Services → Returns Dashboard.

- Late filing attracts penalties under Section 47 of the CGST Act.

Role of Form GSTR-6A

Though Form GSTR-6A is auto-generated and read-only, it serves as a draft statement of inward supplies from suppliers, helping ISDs reconcile ITC before entering details in Form GSTR-6.

When to Use What? Practical Scenarios

Use ISD When:

- Multiple units receive common third-party services (like marketing, advisory, IT) via the head office.

- RCM-paid services such as legal or security services are shared among branches.

- From April 1, 2025 onward, ISD is compulsory for such shared services.

Use Cross Charge When:

- Services or goods are supplied internally (e.g., IT support, equipment) and billed between units.

- Recovery of costs is purely internal, with proper documentation and valuation.

- These remain valid post-April 2025 for internally generated costs.

Example Scenarios:

- A corporate office pays for software licenses used by branches credit distribution should go via ISD.

- An internal HR support team charges branches via invoice cross charge is appropriate here if they’re only providing internal services.

Risks of Non-Compliance

- Denial of ITC: If ISD is not used where required, recipient units may lose eligible ITC.

- Penalties & Litigation: Non-registration or failure to file GSTR-6 can attract notices, interest, and penalties.

- Audit Discrepancies: Misallocation of ITC or misuse of cross-charge could result in scrutiny during audits.

Actionable Takeaways

- Assess your structure: Identify shared service invoices and internal cost flows.

- Register as ISD: If you haven’t already, ensure your head office has obtained ISD registration, as the mandate has been effective since April 1, 2025.

- Update systems: Modify your ERP/invoicing to issue ISD invoices as per Rule 54 and capture distribution details.

- Adopt GSTR-6 filing discipline: Ensure monthly reconciliation via GSTR-6A and accurate filing by the 13th.

- Educate teams: Communicate the distinction and train staff to avoid misclassification of services.

- Document meticulously: Maintain SOPs, standard agreement formats, and logs of ITC distribution.

Conclusion

While ISD and Cross Charge might appear similar, they cater to distinct tax and operational scenarios. With the GST mandate on ISD registration already in effect from April 2025, businesses must comply without delay—registering properly, filing GSTR-6 diligently, and ensuring ITC is distributed correctly. This disciplined approach ensures compliance, optimizes tax recovery, and safeguards against future penalties.