.svg)

RCM on Rent and Sponsorship Services under GST: Complete Guide for 2025

The Reverse Charge Mechanism (RCM) is a unique feature under GST that reverses the tax liability from the supplier to the recipient. While most services fall under forward charge, specified services like renting of motor vehicles and sponsorship services fall under RCM under certain conditions. However, many businesses still remain unclear about how and when to apply RCM on rent, especially on vehicle hire and the often-overlooked intricacies of RCM on sponsorship services.

This blog breaks down the applicability of RCM on rent and RCM on sponsorship services, related GST rules, Input Tax Credit (ITC) eligibility, practical examples, and compliance essentials for 2025.

What is RCM in GST?

Under the normal GST structure, the supplier is responsible for paying the tax. But under the Reverse Charge Mechanism (RCM), the liability shifts to the recipient of goods or services.

RCM is primarily used to cover tax leakages in high-risk sectors or where suppliers are unregistered or difficult to track. Notable services under RCM include:

- Renting of motor vehicles (under specific conditions)

- Sponsorship services

- Legal services

- Goods transport agency (GTA) services

RCM on Renting of Motor Vehicle: Applicable Scenarios

RCM on rent applies only when:

- The supplier of motor vehicle is not a body corporate (e.g., a proprietorship or partnership firm)

- The recipient is a body corporate (e.g., a private limited company)

- The motor vehicle is hired for transportation of passengers

- The supplier is not charging GST under forward charge

These conditions were notified via Notification No. 13/2017 – Central Tax (Rate) and further clarified in subsequent amendments. The RCM on rent effective date is 1st October 2019.

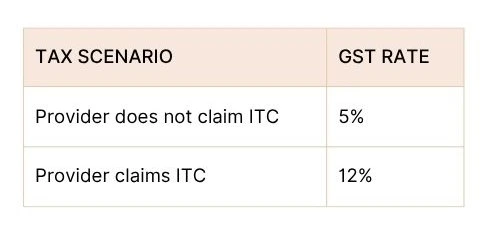

GST Rate under RCM on Renting of Motor Vehicle

Under RCM, the recipient pays tax at the applicable rate and may claim ITC subject to eligibility under Section 16 and non-blocking under Section 17(5) of CGST Act.

Compliance Checklist for RCM on Rent (2025 Ready)

- Verify Supplier Type: Confirm if the vendor is a body corporate or not.

- Check Purpose: Ensure it’s for passenger transport, not goods or other purposes.

- Pay RCM via Cash Ledger: Discharge liability in GSTR-3B under “RCM Liabilities.”

- Claim ITC: If eligible, claim input tax credit in the same month.

- Maintain a Clear RCM Liability/ITC Statement: Essential for audit trail and 2A/2B reconciliation.

RCM on Sponsorship Services: Detailed Overview

What Are Sponsorship Services?

Sponsorship services involve promotional payments made to event organizers, NGOs, sports associations, media platforms, etc., in exchange for brand exposure or event association. These services are taxed under RCM when certain criteria are met.

RCM on Sponsorship Services: When Does It Apply?

As per Notification No. 13/2017 – Central Tax (Rate), RCM on sponsorship services applies when the recipient is:

- A body corporate or

- A partnership firm

and the supplier is any entity (registered or unregistered), such as:

- A sports federation

- NGO or charitable trust

- Event management agency

The corporate or partnership firm receiving sponsorship benefits must pay GST under RCM.

RCM Sponsorship Example:

Company ABC Pvt Ltd sponsors an event organized by a sports club.

- Sports club is the service provider

- Company ABC is the recipient (body corporate)

- RCM applies. Company ABC must pay GST and may claim ITC.

Sponsorship RCM Exemptions and Clarifications

- Services to Government-recognized sporting events by National Sports Federations may be exempt.

- Sponsorship provided to individuals or non-business entities does not attract RCM.

- If the recipient is not a body corporate or partnership, RCM is not applicable (e.g., individuals or sole proprietors receiving sponsorship do not trigger RCM).

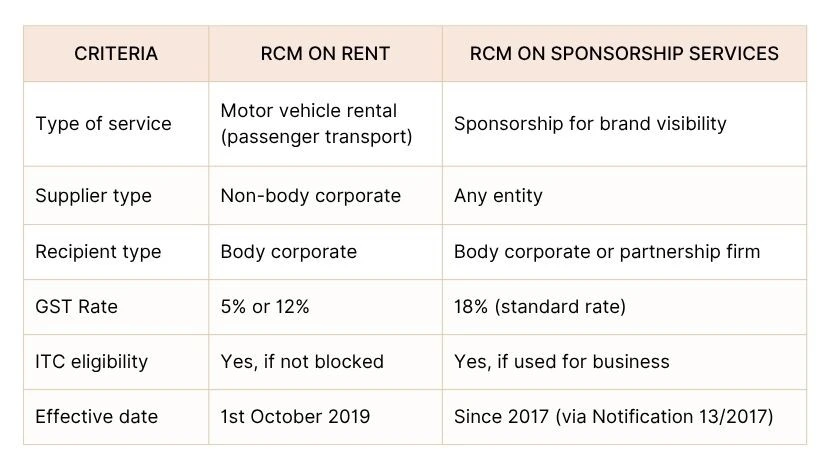

Key Differences Between RCM on Rent vs RCM on Sponsorship

Common Mistakes in RCM Compliance

- Treating all rental invoices as under forward charge

- Missing RCM on small-value vehicle hires

- Incorrect entity type verification in sponsorship transactions

- Delayed ITC claim or non-reporting in GSTR-3B

- Not reconciling RCM transactions with GSTR-2B

How to Ensure Smooth RCM Compliance in 2025

Use GST automation tools like CashFlo to:

- Automatically flag RCM-applicable transactions

- Generate separate RCM liability/ITC statements

- Push entries into GSTR-3B and 2B for real-time reconciliation

Train your AP team to:

- Differentiate between forward and reverse charge services

- Verify vendor registration and entity status

- Maintain audit-ready documentation

Frequently Asked Questions

Q1: Is RCM applicable on rent paid to registered vehicle rental companies?

A: No, if the supplier is a body corporate and charging GST, RCM is not applicable.

Q2: Can we claim ITC on GST paid under RCM for rent or sponsorship?

A: Yes, provided the services are used for business purposes and not restricted under Section 17(5).

Q3: Is RCM applicable on sponsorship paid to individuals or NGOs?

A: RCM is not applicable if the recipient is an individual. It is applicable if the recipient is a body corporate or partnership and the service provider is any entity.

Conclusion:

Whether it's RCM on rent under GST or RCM on sponsorship services, accurate classification and compliance are key to avoiding penalties in 2025. With growing scrutiny from tax authorities and real-time GST data matching, businesses must stay proactive. Automate where possible, review notifications regularly, and always check the applicability based on supplier-recipient structure.

.webp)