.svg)

TDS Under GST in India: Rules, Procedures, and Compliance Guide

The Goods and Services Tax (GST) has reshaped India’s indirect taxation by bringing uniformity and reducing tax complexities. To strengthen this system further, mechanisms like Tax Deducted at Source (TDS) were introduced. TDS under GST ensures that tax is collected right at the time of making payments for certain supplies, helping the government curb tax evasion and improving cash flow in the system.

Unlike income tax TDS, which individuals and businesses encounter on salaries, contracts, and professional fees, TDS under GST is restricted to specific entities such as government departments, local authorities, and public sector undertakings. These entities, while making payments to suppliers for taxable supplies, must deduct a small percentage of the invoice value as tax and remit it to the government.

In this guide, we’ll dive deep into the rules, applicability, rates, procedures, compliance steps, and practical aspects of TDS under GST.

What Does TDS Under GST Mean?

TDS in GST is covered under Section 51 of the CGST Act, 2017. The law mandates that notified entities must deduct tax at source when making payments to suppliers for taxable goods and services.

This deduction is a fixed percentage of the taxable value (excluding GST and cess) and is required only when the payment amount under a single contract crosses the threshold limit. Once deducted, the amount must be deposited with the government, and the supplier gets the benefit of the deduction as credit in their electronic cash ledger.

Entities Required to Deduct TDS Under GST

Not everyone falls under the ambit of GST TDS. The law specifically notifies certain categories of entities, typically those linked with the government. These include:

- Central and State Government departments and ministries

- Local authorities and municipal bodies

- Governmental agencies formed under law

- Boards and statutory bodies created by Parliament or State Legislatures, where the government holds at least 51% equity or control

- Societies formed by government bodies and registered under the Societies Registration Act

- Public Sector Undertakings (PSUs)

It’s worth noting that not all transactions involving these entities are subject to TDS. For example, supplies between PSUs or certain inter-departmental transactions may be exempt from this provision.

When Is TDS Applicable Under GST?

The applicability of TDS depends on the value of the contract and the nature of the transaction. Here are the key triggers:

- Exclusion of GST in Calculation:

TDS is deducted on the taxable value of supply only. That means the CGST, SGST, IGST, or cess components mentioned separately in the invoice are not considered for TDS computation. - Place of Supply Exception:

If the supplier states and places of supply are different from the recipient's state of registration, TDS is not required. This exception avoids complications in transferring state-specific GST (SGST) across jurisdictions.

Prescribed Rate of TDS Under GST

A TDS rate of 2% is currently applied under GST to the taxable value.

- Intra-State Supply (within one state):

- 1% CGST + 1% SGST

- 1% CGST + 1% SGST

- Inter-State Supply (between two states):

- 2% IGST

This simple rate structure makes it easy for deductors to calculate the exact TDS amount.

Step-by-Step Compliance Timeline for GST TDS

To comply with GST TDS provisions, deductors must follow a series of steps from registration to certificate issuance:

1. Registration

Entities required to deduct TDS must obtain a GST registration specifically as a TDS deductor. This can be done using their TAN (Tax Deduction Account Number), even if they do not possess a PAN.

2. Deduction of TDS

When making payment or crediting the supplier, the deductor must withhold 2% of the taxable value.

3. Deposit of TDS

Deposits must be made with the government within 10 days after the deduction occurs.

4. Filing of Return (GSTR-7)

Form GSTR-7 must be filed by the 10th of the following month by every deductor. This return contains details of all TDS deductions for that period.

5. Issuing TDS Certificate

To issue a TDS Certificate, the deductor must submit Form GSTR-7A to the supplier within five days of depositing the tax. This certificate acts as proof of deduction and enables the supplier to claim credit.

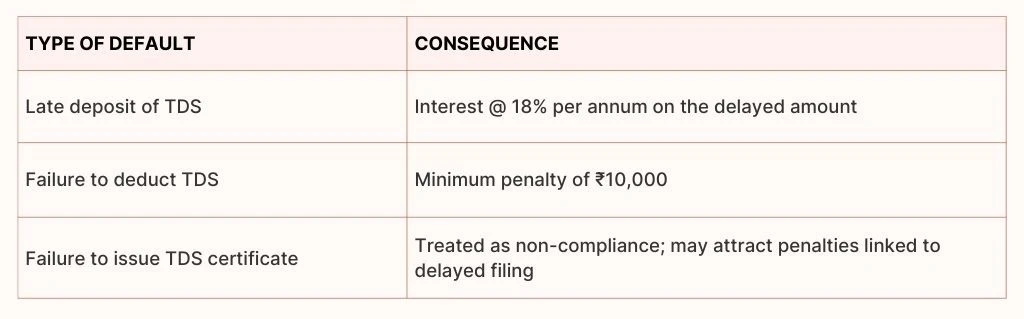

Penalties and Consequences for Non-Compliance

Non-compliance with TDS provisions can result in strict penalties and interest.

Thus, timely deduction, deposit, and reporting are essential to avoid unnecessary costs and litigation.

Benefits for Suppliers

While the onus of compliance rests on the deductor, suppliers also benefit from GST TDS:

- Deducted amounts are recorded in the supplier's electronic cash ledger.

- This credit can be seamlessly used for paying future GST liabilities, interest, or penalties.

- There is no need to manually submit TDS certificates—the credit appears automatically in Form GSTR-2A.

This system ensures that suppliers are not financially burdened by TDS; instead, it acts as an advance deposit toward their tax liability.

Recent Amendments and Updates

The GST TDS mechanism has seen several updates to improve efficiency:

- Invoice-Level Reporting in GSTR-7:

From April-2025, deductors must report detailed information such as invoice numbers, taxable value, and GST components while filing GSTR-7. - Compulsory Filing Even with Nil Deduction:

Effective January 2024, GSTR-7 must be filed every month even if no TDS is deducted during that period. - Exclusion of GST Component from TDS:

The CBDT clarified that TDS should not be deducted on GST amounts separately mentioned in invoices only on the base taxable value.

Why Is TDS Under GST Important?

- For the Government:

- Ensures continuous revenue inflow

- Improves tax discipline and reduces evasion

- Strengthens data accuracy in returns

- Ensures continuous revenue inflow

- For Suppliers:

- Provides a ready cash ledger balance

- Reduces compliance burden due to automatic credit reflection

- Provides a ready cash ledger balance

- For Businesses/ Deductors:

- Builds transparency in operations

- Helps avoid future disputes and audits when handled properly

- Builds transparency in operations

Common Mistakes and How to Avoid Them

Pitfalls:

- Not registering as a TDS deductor despite eligibility

- Overlooking the ₹2.5 lakh threshold condition

- Deducting TDS on the total invoice value including GST instead of taxable value

- Delayed deposits or forgetting to issue certificates

- Missing GSTR-7 filing deadlines

Best Practices:

- Keep a checklist of contracts above the threshold limit

- Automate payment and filing reminders for TDS deposits

- Train finance teams on identifying place-of-supply exceptions

- Regularly reconcile deductions with supplier ledgers to ensure accuracy

- Communicate proactively with suppliers about deductions and certificate availability

Conclusion

TDS under GST is more than just a compliance requirement; it is a critical tool that strengthens the GST ecosystem. By mandating tax deduction at source, the government ensures steady revenue collection while giving suppliers a transparent way to claim credits.

For businesses and government bodies, timely compliance with TDS provisions not only avoids penalties but also builds confidence in their operations. On the other hand, suppliers benefit through the automatic credit system, making the process hassle-free.

As GST compliance continues to evolve, staying vigilant about updates like mandatory invoice-level reporting in GSTR-7 and compulsory nil returns is essential. A robust understanding and disciplined implementation of GST TDS can help entities achieve smooth compliance while contributing to a transparent taxation environment.

.webp)