.svg)

How Aggregate Turnover Affects Your GST Liability

The Goods and Services Tax (GST) system introduced in India was designed to simplify indirect taxation and create a unified national tax structure. However, several technical concepts within GST can significantly affect a business’s tax obligations. One of the most important among them is aggregate turnover.

Many businesses assume that GST liability depends only on taxable sales. In reality, GST registration and compliance obligations are determined based on aggregate turnover, a broader concept that includes multiple types of supplies.

Understanding how aggregate turnover is calculated and how it impacts GST liability is essential for businesses of all sizes. Misinterpreting this definition can result in delayed GST registration, penalties, and compliance issues.

This article explains the concept of aggregate turnover, what is included in it, what is excluded, and how it directly affects GST liability for businesses in India.

Understanding Aggregate Turnover Under GST

The definition of aggregate turnover is provided under Central Goods and Services Tax Act, 2017.

According to Section 2(6) of the Act, aggregate turnover means the total value of all supplies made by a person across India under the same Permanent Account Number (PAN) during a financial year.

Aggregate turnover includes:

- Taxable supplies of goods or services

- Exempt supplies

- Export of goods or services

- Inter-state supplies between branches having the same PAN

However, the calculation excludes GST taxes such as CGST, SGST, IGST, and compensation cess.

Another important aspect is that aggregate turnover is calculated on an all-India basis, meaning businesses must combine the turnover of all their branches or units operating under the same PAN across different states.

This broader definition makes aggregate turnover a crucial factor in determining GST obligations.

GST Registration Threshold Based on Aggregate Turnover

One of the primary impacts of aggregate turnover is determining whether a business must register under GST.

Under Section 22 of the CGST Act, a business must obtain GST registration if its aggregate turnover exceeds the prescribed threshold limit in a financial year.

The current threshold limits are:

- ₹40 lakh – for businesses supplying goods in most states

- ₹20 lakh – for service providers

- ₹20 lakh or ₹10 lakh – for certain special category states depending on the nature of supply

For example:

- If a trader dealing in goods crosses ₹40 lakh turnover, GST registration becomes mandatory.

- If a consultancy firm providing services crosses ₹20 lakh turnover, GST registration is required.

Businesses that fail to register after crossing these limits may face penalties and tax liabilities for unreported supplies.

Components Included in Aggregate Turnover

To determine whether a business crosses the GST threshold limit, several types of supplies must be included when calculating aggregate turnover.

1. Taxable Supplies

Taxable supplies refer to goods or services that attract GST at applicable rates such as 5%, 12%, 18%, or 28%.

These supplies represent the primary revenue-generating transactions of a business and must always be included in aggregate turnover.

For example, if a manufacturer sells products worth ₹25 lakh in a financial year, the entire amount contributes to aggregate turnover.

2. Exempt Supplies

One common misconception is that exempt supplies are not counted in turnover. However, GST law clearly states that exempt supplies must also be included in aggregate turnover calculations.

Exempt supplies include:

- Goods or services attracting nil GST rate

- Supplies fully exempt through government notifications

- Non-taxable supplies such as alcoholic liquor for human consumption

Even though GST is not charged on these transactions, their value still contributes to aggregate turnover.

3. Export of Goods and Services

Exports are classified as zero-rated supplies under GST.

This means exporters can claim input tax credit or refunds even though GST is not charged on exports.

Despite being zero-rated, export turnover must still be included while calculating aggregate turnover.

For example, if a software company exports services worth ₹12 lakh, this amount will form part of its aggregate turnover.

4. Inter-State Supplies

Supplies made between different states under the same PAN must also be included in aggregate turnover.

For instance, if a company has offices in Maharashtra and Karnataka and transfers goods between them, these transactions count toward aggregate turnover.

This rule ensures that businesses cannot avoid GST registration by splitting operations across different states.

Transactions Excluded from Aggregate Turnover

While many supplies are included in aggregate turnover, certain elements must be excluded.

These include:

- GST taxes collected from customers (CGST, SGST, IGST, and cess)

- Inward supplies on which tax is paid under the Reverse Charge Mechanism (RCM)

- Pure purchase transactions made by the business

These exclusions ensure that aggregate turnover reflects the actual value of outward supplies rather than taxes collected on behalf of the government.

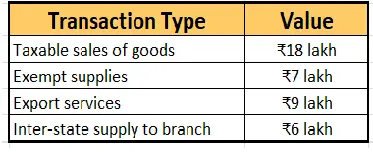

Practical Example of Aggregate Turnover Calculation

Understanding aggregate turnover becomes easier with a practical example.

Consider a business with the following transactions during a financial year:

Aggregate Turnover = ₹40 lakh

In this scenario:

- The business has crossed the ₹40 lakh threshold applicable to suppliers of goods.

- Therefore, the business must register under GST.

Even though exempt supplies and exports do not attract GST, they still contribute to aggregate turnover.

How Aggregate Turnover Affects GST Liability

The definition of aggregate turnover has several direct implications for businesses.

1. Determining Mandatory GST Registration

The most immediate impact is whether a business must obtain GST registration.

Once the aggregate turnover crosses the applicable threshold, the business must:

- Apply for GST registration

- Start charging GST on taxable supplies

- File GST returns regularly

Failure to do so can result in penalties and interest on unpaid taxes.

2. Eligibility for the Composition Scheme

Aggregate turnover also determines eligibility for the GST Composition Scheme, which is designed for small taxpayers.

Businesses with turnover up to ₹1.5 crore may opt for the composition scheme, allowing them to pay tax at a lower rate with simplified compliance requirements.

However, once the aggregate turnover exceeds this limit, the business must shift to the regular GST scheme.

3. Impact on Compliance Requirements

As aggregate turnover increases, businesses may face additional compliance obligations such as:

- Filing regular GST returns

- Maintaining detailed accounting records

- Implementing GST-compliant invoicing systems

- Meeting e-invoicing requirements if turnover exceeds specified thresholds

Thus, aggregate turnover not only determines registration but also influences the overall compliance burden.

Common Mistakes Businesses Make

Many businesses make errors while calculating aggregate turnover. These mistakes can lead to incorrect GST compliance decisions.

Ignoring Exempt Income

Businesses often assume that exempt supplies are irrelevant for GST calculations. In reality, they must be included in aggregate turnover.

Not Combining Turnover Across States

Businesses operating in multiple states sometimes calculate turnover separately for each branch. However, GST requires PAN-based all-India turnover calculation.

Including GST in Turnover

GST collected from customers should not be counted as turnover since it represents tax collected for the government.

Overlooking Inter-State Supplies

Branch transfers and inter-state transactions must be included in aggregate turnover even if they occur within the same company.

Best Practices for Businesses

Businesses can manage GST compliance more effectively by following a few best practices:

Monitor turnover regularly

Track revenue monthly to identify when the threshold limit is approaching.

Maintain proper records

Accurate records of taxable, exempt, and export supplies help ensure correct turnover calculation.

Use GST-enabled accounting software

Automation tools simplify GST compliance and reduce calculation errors.

Consult tax professionals

Professional advice helps businesses understand regulatory requirements and avoid penalties.

Conclusion

Aggregate turnover is a key concept in GST that determines a business’s registration requirements, eligibility for schemes, and compliance obligations. Because the definition includes taxable supplies, exempt supplies, exports, and inter-state transactions, businesses must calculate turnover carefully.

Misunderstanding aggregate turnover can lead to delayed GST registration, financial penalties, and operational complications. By maintaining proper records, monitoring turnover regularly, and understanding the GST rules clearly, businesses can ensure smooth compliance and avoid unnecessary risks.

Ultimately, a clear understanding of aggregate turnover not only helps businesses meet GST requirements but also supports better financial planning and tax management.