.svg)

GST on Pharmaceuticals: Rates, Exemptions & HSN Explained

India’s pharmaceutical sector is one of the world’s largest producers of affordable medicines, vaccines, and healthcare products.

Since the introduction of the Goods and Services Tax (GST) in 2017, the sector has witnessed a major tax transformation. GST replaced a complex web of levies such as excise duty, VAT, and service tax with a unified system that ensures transparency and efficiency.

For pharmaceutical companies, distributors, and hospitals, understanding GST’s rate structure, exemptions, and HSN classifications is crucial for maintaining compliance and controlling costs.

GST Council’s Continued Efforts Toward Affordable Healthcare

In its 56th GST Council Meeting, the government took key steps to simplify taxation and make essential healthcare more affordable:

- 37 life-saving drugs were granted full GST exemption.

- Most other pharmaceutical products were moved under a uniform 5% GST slab.

- HSN classifications were rationalised to eliminate interpretational disputes.

These measures reflect a clear policy direction — ensuring access to essential medicines while maintaining fair tax governance.

Overview of GST Rate Structure for Medicines and Healthcare Goods

Under GST, pharmaceutical goods are classified into four main tax slabs — Nil, 5%, 12%, and 18%, based on their use, necessity, and type.

While life-saving drugs enjoy exemptions, specialised formulations and non-essential medical goods attract higher rates. This multi-tier structure balances affordability with fiscal responsibility.

Zero GST on Life-Saving and Essential Medicines — Ensuring Affordability for All

To promote public health and affordability, the government has exempted several critical medicines and biological products from GST altogether.

These include drugs and vaccines used for treating serious diseases like cancer, HIV/AIDS, tuberculosis, and chronic kidney ailments.

The Nil rate ensures that life-saving treatments remain accessible and free from indirect tax burdens.

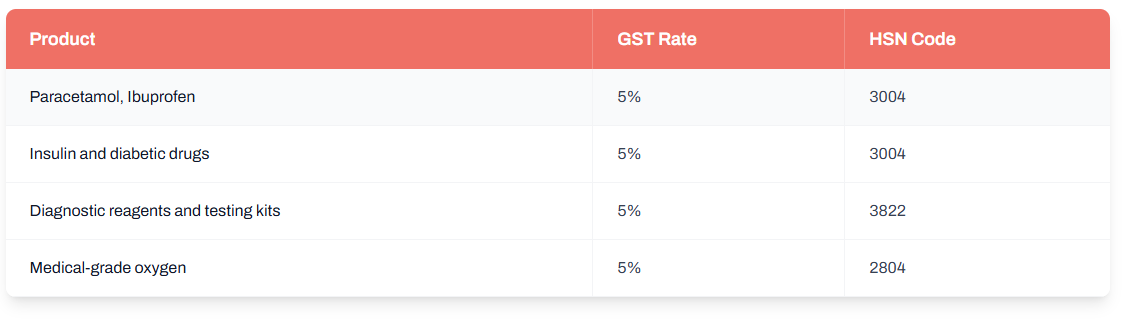

Low 5% GST on Common Medicines and Healthcare Products — Balancing Affordability with Revenue

Most commonly prescribed medicines and basic healthcare goods fall under the 5% GST bracket. This includes antibiotics, pain relievers, insulin, and essential medical supplies.

This 5% rate has streamlined compliance for chemists and distributors while keeping medicine prices stable for patients.

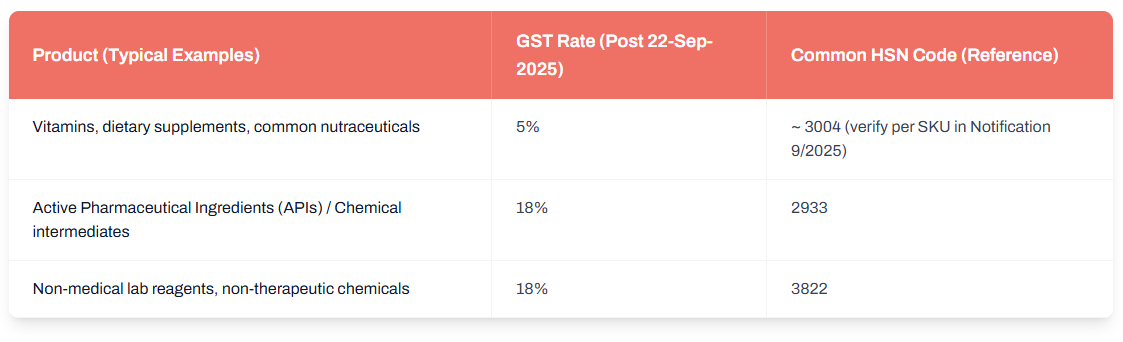

Higher 5% and 18% GST Slabs — For Nutraceuticals, APIs & Non-Therapeutic Consumables

With the GST Council’s rationalisation effective 22 September 2025, the previous 12% slab for many pharmaceutical and nutrition-oriented products has been replaced. Here is the updated rate structure:

- Finished medicines, nutraceuticals, and vitamin formulations: Many of these have now been moved to a 5% GST slab, down from 12%. This applies to a broad range of dietary supplements and common drug formulations.

- Active Pharmaceutical Ingredients (APIs), KSMs, and chemical intermediates: These continue to attract 18% GST, reflecting their industrial and non-retail-character.

- Non-therapeutic lab reagents and consumables: Items like non-medical chemicals, laboratory reagents, and other non-therapeutic consumables also fall under the 18% slab.

Here is an updated reference table for clarity (based on the Notification 9/2025-CT(Rate) list):

Why this change matters:

- Moving many finished medicines and nutraceuticals to 5% ensures they remain affordable and reduces tax burden on end consumers.

- Applying 18% to APIs and intermediates preserves tax revenue since these are largely industrial inputs rather than retail products.

- Imposing 18% on non-therapeutic lab consumables ensures that goods not directly used for patient treatment contribute appropriately to GST collections.

Important Compliance Note:

For item-level classification and rate checks, businesses must rely on Notification 9/2025-CT (Rate), which provides the consolidated HSN-wise GST rate list. During the transition, companies should verify their SKUs against this notification to ensure correct billing, tax collection, and Input Tax Credit (ITC) treatment.

GST on Medical and Hospital Services — Understanding Exemptions and Taxable Cases

Most core healthcare services are exempt under Notification No. 12/2017–Central Tax (Rate). However, not all medical activities fall within this exemption.

- Exempt Services:

- Hospitalisation, diagnostics, and surgeries for illnesses or injuries.

- Services provided by doctors, nurses, and registered hospitals.

- Hospitalisation, diagnostics, and surgeries for illnesses or injuries.

- Taxable Services:

- Cosmetic or aesthetic surgeries not linked to treatment.

- Hospital room rent exceeding ₹5,000 per day (for non-ICU rooms) taxed at 5% without ITC.

- Cosmetic or aesthetic surgeries not linked to treatment.

Critical care and ICU facilities remain fully exempt to protect patients from unnecessary cost escalation.

GST on Hospitalisation Packages — How Composite Healthcare Billing Is Treated

Hospitals often provide bundled packages combining treatment, stay, and diagnostic services. Under GST, such packages are treated based on the “principal supply” concept:

- If the dominant component is healthcare, the entire package is exempt.

- If non-medical amenities are included (like spa or luxury stays), a portion may become taxable.

Accurate classification and billing are vital for hospitals to avoid GST disputes.

Determining the Value of Supply — How GST on Medicines Is Computed

The value of supply forms the base for GST calculation in pharmaceuticals.

It includes:

- The transaction value charged to buyers.

- Discounts reflected on invoices.

- Credit notes for returned goods.

- Free samples, where ITC reversal is mandatory.

Manufacturers must ensure correct valuation to avoid mismatched reporting in GSTR-1, GSTR-3B, and GSTR-2B filings.

GST on Import of Pharmaceutical Goods and APIs — Compliance for Importers

India imports a significant portion of its APIs and formulations. Imported medicines attract:

- IGST at the same rate applicable to domestic goods, and

- Basic Customs Duty (BCD) as per customs laws.

Importers can claim input tax credit (ITC) on IGST paid if the goods are used for taxable supplies.

However, life-saving drugs imported under government or charitable programs may be exempt through specific notifications.

Treatment of Expired or Returned Medicines under GST — ITC Reversal and Credit Notes

Pharmaceutical manufacturers and distributors frequently deal with expired or returned stock.

Under GST law:

- Returned medicines allow suppliers to issue a credit note to adjust output tax.

- Destroyed or expired goods require ITC reversal under Section 17(5)(h) of the CGST Act.

Accurate documentation and reconciliation ensure smooth audits and maintain input credit accuracy.

HSN Codes and Classification — The Backbone of Pharmaceutical GST Compliance

Each medicine, chemical, or medical device falls under a specific HSN (Harmonised System of Nomenclature) code, which determines the correct tax rate and reporting requirements.

Common HSN Codes Used in Pharma Sector:

- 3002: Blood, plasma, and vaccines

- 3003 / 3004: Medicaments and formulations

- 2933: Active Pharmaceutical Ingredients (APIs)

- 3822: Diagnostic kits and reagents

Correct classification avoids penalties and ensures smooth cross-border trade and GST return filing.

Impact of GST on the Pharmaceutical Industry — Simplified Compliance and Transparency

The introduction of GST has significantly improved operational efficiency across the pharmaceutical supply chain:

- Unified Taxation: One national tax replaced multiple overlapping levies.

- Reduced Logistics Costs: Elimination of state barriers streamlined distribution.

- Stable Pricing: Removal of cascading taxes helped maintain medicine affordability.

- Improved Credit Flow: Input credits are now traceable and transparent.

The rationalisation announced by the 56th GST Council continues this trend, reducing compliance friction and supporting the healthcare sector’s growth.

Conclusion

The GST system has redefined taxation for India’s pharmaceutical industry by balancing affordability with accountability.

By exempting essential drugs, rationalising rates, and clarifying HSN codes, GST ensures both public health protection and business transparency.

For manufacturers, hospitals, and distributors, staying informed about rate notifications, exemptions, and ITC rules is key to smooth compliance. As the government continues to refine GST for the healthcare sector, the future points to a more unified, efficient, and affordable system for all stakeholders.

.webp)